Earnin is a legitimate earned wage access (EWA) app that lets you tap into money you've already earned before payday arrives. The app charges no interest, requires no credit checks, and operates on a voluntary tipping model—making it fundamentally different from payday loans. With overwhelmingly positive user reviews, Earnin has built a solid reputation as a safe financial tool. That said, the app works best for people with consistent paychecks, direct deposits, and stable employment who need short-term cash flow help between pay periods. Here’s what you need to know and a full Earnin review for you.

What Is Earnin?

Earnin is a fintech app that allows workers to access a portion of their earned wages before their official payday. Unlike traditional payday loans or credit-based cash advance services, Earnin doesn't lend you money—it gives you access to pay you've already earned through work. The app is designed for employees with regular paychecks and direct deposit, offering a way to bridge gaps when bills and paychecks don't line up.

Here is how the company operates: you connect your bank account and employment information, and Earnin calculates how much you've earned so far in your current pay period. You can then request access to those earnings instantly or on a faster timeline, and Earnin handles the transfer. There's no interest charged, no mandatory fees, and no credit check required. Instead, users have the option to leave a voluntary tip—the amounts completely up to you.

Key Features of Earnin

Earnin's main strength lies in its feature set, which goes beyond simple cash advances.Here are its key features:

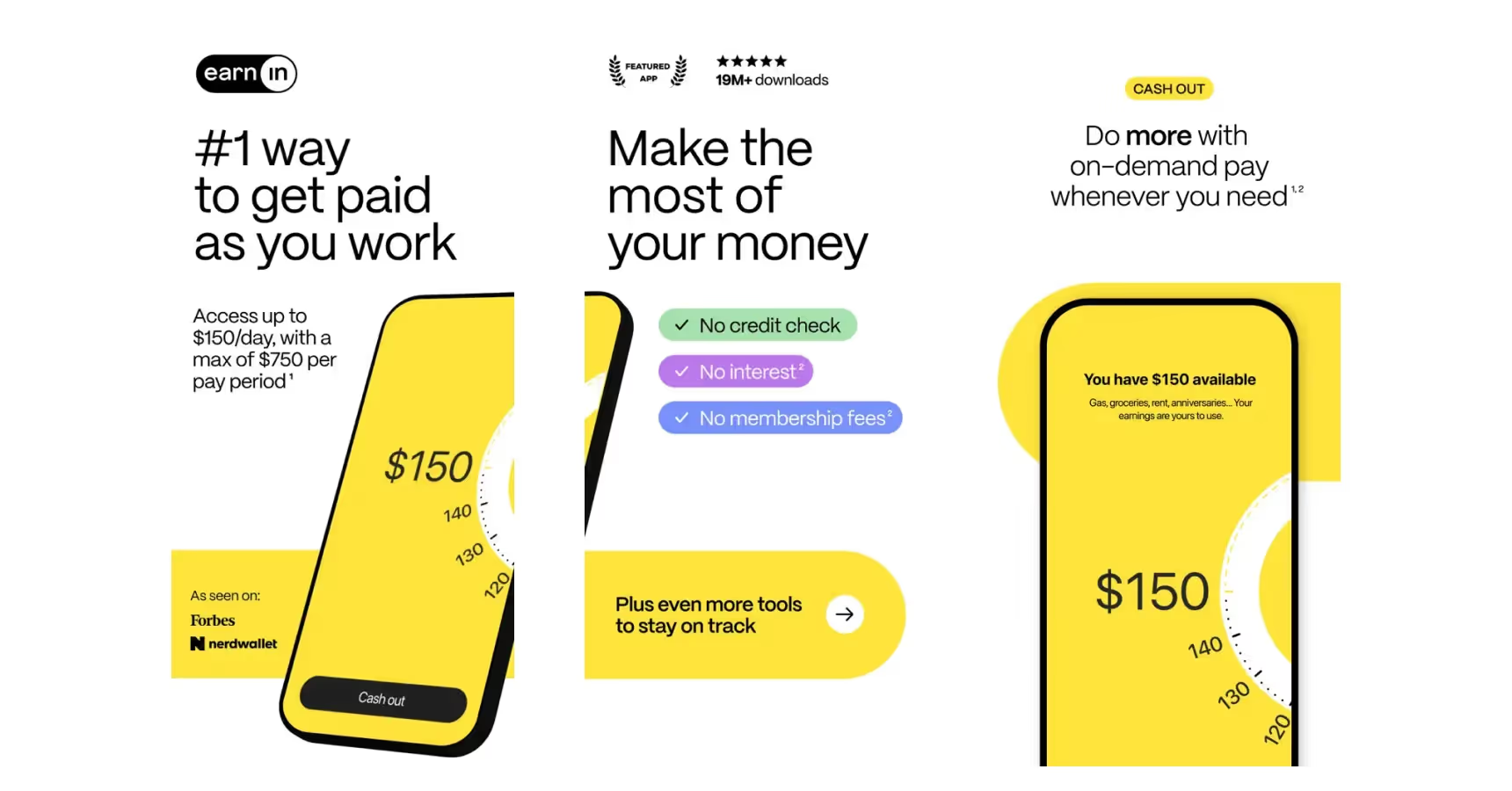

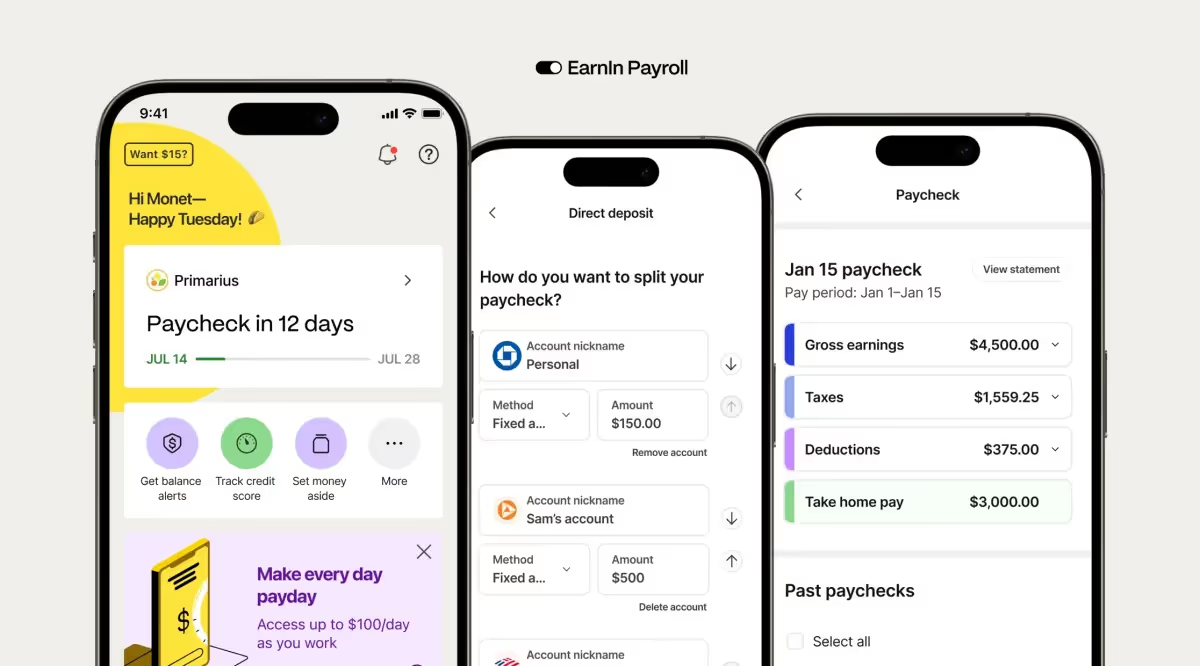

- Cash Out lets you access up to $150 per day, with a maximum of $1,000 per pay period, with standard transfers free and arriving in 1–2 business days. Lightning Speed expedites this to minutes for a fee if you need funds urgently.

- Early Pay is another valuable feature—it gets your full paycheck to you up to two days before your scheduled payday.

- Balance Shield sends low-balance alerts and can automatically transfer funds to help prevent overdrafts.

- Tip Yourself lets you save money directly within the app, setting aside up to $100 per day across multiple savings jars.

- Live Pay, powered by the EarnIn Card, is their newest innovation, allowing real-time pay access as you work, enabling up to $1,500 per pay period for eligible users.

How Does Earnin Work?

Using Earnin starts with downloading the app and verifying your employment and banking details. The app needs to confirm your direct deposit history to calculate how much you've earned. Once verified, you'll see your available balance—the amount of money you've already earned but haven't received yet.

Earnin’s Verification Process

When you first sign up, you'll need to provide several pieces of information. Your employer details, pay schedule, and work location help Earnin verify you're a legitimate employee earning regular paychecks. You'll also connect your bank account through Plaid, a secure financial data link that's widely used across fintech apps.

Here's the important part: Earnin doesn't give you access immediately. Most new users need to wait through two pay cycles before their first withdrawal becomes available. This waiting period allows Earnin to verify your employment information and confirm your pay schedule matches what you reported. It sounds inconvenient, but it's a safety mechanism that prevents fraud and protects both you and the company.

How to Request Cash Out

Once you're verified and eligible, requesting money is simple. Open the app, select how much you want to access (up to your daily and pay-period limits), and choose your transfer speed. Standard transfers are free but take 1–2 business days. Lightning Speed costs a fee but delivers funds in minutes.

The money comes directly from your future paycheck. When payday arrives, Earnin automatically deducts what you withdrew plus any optional tips or Lightning Speed fees. If you used Balance Shield transfers or Early Pay, those also come out automatically. The beauty of this system is there's no separate repayment schedule—it all happens on payday without extra effort.

Earinin’s Eligibility Requirements

Not everyone qualifies for Earnin. You need to be 18 or older, live in the United States (with the exception of Connecticut), and have a valid US cellphone number. Professionally, you need consistent employment with a regular paycheck and direct deposit. Your employer must deposit at least $350 per pay period, and more than 50% of that deposit must go to a checking account (not savings).

You also need either a fixed work location that you can verify or a work email address. Gig workers and freelancers don't qualify unless they have regular, verifiable income through a connected platform. Self-employed individuals typically can't use Earnin because the app can't reliably verify their income.

Why Earnin Is Legit?

Multiple factors confirm Earnin's legitimacy. The app is backed by real venture capital funding and operates as a licensed financial technology company. It's regulated by state and federal authorities, and the company maintains compliance with banking regulations. Earnin partners with established banks like Evolve Bank & Trust and Lead Bank—both FDIC members—to hold deposits and process transfers safely.

User Reviews and Ratings

Real users provide strong evidence of Earnin's legitimacy. On Trustpilot, Earnin holds a 4.8 out of 5 rating based on thousands of reviews. Users consistently praise the app's simplicity, quick transfers, and responsive customer service. Common themes in positive reviews include avoiding overdraft fees, covering rent during tight months, and managing unexpected expenses without going into debt.

"I highly recommend Earnin if you are struggling to get by every two weeks," one user wrote. "It's especially hard being single with no help. Thanks to Earnin, I don't have to eat peanut butter and jelly sandwiches for dinner in between paychecks."

Another user highlighted customer service: "They have helped me with my bills and being on time on rent. I can't say what would happen without them."

Expert Recognition

Major financial publications have reviewed and endorsed Earnin. Forbes Advisor notes that Earnin is best suited for people needing emergency cash between paychecks who have fixed work locations and direct deposits. MarketWatch highlights Earnin's optional tip model and points out that users typically spend advances on necessities like groceries, gas, and rent—not frivolous purchases.

These third-party validations matter because they come from sources with no stake in promoting Earnin. They provide unbiased analysis based on the app's actual features and user experiences.

What Can You Use Earnin For?

Users leverage Earnin for a wide variety of needs, but certain uses are far more common than others. The app shines when you need to cover essential expenses that fall between paychecks.

Common Use Cases

Covering rent and utilities is the single biggest use case. Workers often find themselves short on rent due to timing issues, and Earnin bridges that gap without late fees or the stress of eviction risk. Groceries and food costs come second—many users describe buying food they couldn't otherwise afford until payday.

Emergency medical costs and unexpected car repairs round out the top uses. The difference between Earnin and other solutions is the speed and lack of debt. You're not taking out a loan; you're accessing money that's already yours.

What Earnin Won't Cover

Earnin works best for genuine financial gaps, not lifestyle upgrades. While you technically can use the money for anything, the app works on an honor system that relies on responsible use. People who consistently max out their daily limits before every payday risk developing a dependency pattern that makes their financial situation worse, not better.

Earnin’s Potential Drawbacks and Concerns

No financial tool is perfect, and Earnin has limitations you should understand before signing up.

Security History

Earnin has experienced two security incidents that users should know about. In February 2019, a third-party security firm accessed sensitive customer data including bank transactions and GPS coordinates. This breach revealed weaknesses in how Earnin handled data from external partners. Earnin addressed the vulnerabilities and tightened protocols, but it raised questions about their oversight.

More recently, in June 2024, Earnin disclosed a cyber incident affecting their banking partner Evolve Bank and Trust. While the breach didn't occur on Earnin's own systems, customer data may have been exposed through the partner's network. Earnin was transparent about the incident and worked with authorities to investigate.

These events highlight a real risk with any app that connects directly to your bank account—your security depends not just on the company's own defenses but on their partners' security too. This doesn't make Earnin illegitimate, but it does mean you should monitor your account and credit regularly.

Limit Restrictions

Your daily and pay-period limits start conservatively when you're new. Most people can access $100 to $150 per day initially, not the full $1,000 per period. Limits increase over time as Earnin builds confidence in your employment history and repayment patterns. This can be frustrating if you need more cash quickly, but it's also a safety feature preventing you from over-borrowing.

Dependency Risk

The biggest potential issue isn't Earnin's fault—it's user behavior. Some people use Earnin every payday, essentially living off advances. This creates a cycle where you're perpetually spending next week's money, making it harder to save or escape the paycheck-to-paycheck trap.

Several Reddit users shared warnings about this: "It's definitely a legitimate service, but it seems you might not be able to access a cash advance quickly enough to assist you at this moment." Another noted: "Be cautious when using early paycheck applications, as it can be simple to get trapped in a pattern of continuously borrowing against your upcoming earnings."

How Earnin Compares to Alternatives

If you're considering Earnin, you likely have other options. Understanding the differences matters.

Earnin vs. Payday Loans

Payday loans charge interest rates of 300% APR or higher, with aggressive repayment terms. You're borrowing money at predatory rates. Earnin's advantage is clear: you're accessing your own wages with no interest and no mandatory fees. That alone makes Earnin fundamentally safer.

Earnin vs. Credit Card Cash Advances

Credit card cash advances carry similar interest rates to payday loans (18% to 35% APR) plus upfront fees. They also impact your credit utilization ratio, potentially damaging your credit score. Earnin doesn't charge interest, doesn't require a credit check, and doesn't affect your credit.

Earnin vs. Other Wage Advance Apps

Apps like Dave, Brigit, and Varo Advance offer similar services but with important differences. Most charge subscription fees ($10 to $20 monthly) or require upgrades to unlock features. Some have smaller daily limits. Dave requires a minimum balance and charges monthly membership fees. Brigit offers free cash advances but up to smaller amounts than Earnin, and their tips are a bit more aggressive.

Earnin's free basic model gives you access without the subscription burden, though you can pay more for faster transfers if needed.

How to Use Earnin Responsibly

Is Earnin legit? Yes. But legitimacy doesn't mean it's right for everyone or suitable for unlimited use.

1. Set Clear Boundaries

Use Earnin as a true safety net for emergencies, not as a regular budgeting tool. If you find yourself using Cash Out every payday, your real problem isn't access to early wages—it's that your expenses exceed your income. Earnin masks the problem but doesn't solve it.

2. Monitor Your Balance

Check your account regularly to see how much you've withdrawn each cycle. Notice if the amounts are increasing. That's a signal you're relying too heavily on advances.

3. Pair Earnin With Budgeting

Use Earnin alongside a budget or app that tracks spending. This helps you see where your money actually goes and makes it easier to identify where you can cut back.

4. Use Balance Shield Strategically

This feature is genuinely useful. Set your low-balance alert at a realistic threshold and let automatic transfers protect you from overdrafts. This prevents the expensive NSF fees that often trap people in financial spirals.

Conclusion

Is Earnin legit? Yes. It's a registered fintech company offering a legal financial service. It doesn't charge interest, doesn't require credit checks, and operates transparently about its fees and features. The company has clear regulatory approval, partners with legitimate banks, and maintains strong user satisfaction ratings.

That legitimacy comes with responsibility on your end. Earnin works best for people with stable paychecks who occasionally need cash before payday, not for people trying to solve chronic cash flow problems. If you meet the eligibility requirements and you use the app sparingly for genuine emergencies, Earnin can be a useful financial tool.

For those looking to build a more sustainable income solution, considering platforms like Alidrop for dropshipping opportunities (if you're interested in supplemental income) can help reduce reliance on wage advances altogether. Alidrop offers a 7-day free trial on its dropshipping plans with access to custom branding, 24/7 VIP customer support, and more.

Is Earnin Legit? FAQs

Does Earnin charge interest or hidden fees?

No. Earnin doesn't charge interest on Cash Out withdrawals or mandatory fees for standard transfers. Lightning Speed transfers cost a fee, and Early Pay has a $2.99 charge, but both are optional and clearly disclosed upfront. Tips are entirely voluntary. Unlike payday loans, there are no hidden charges or surprise costs that appear later.

Will using Earnin hurt my credit score?

Not at all. Earnin doesn't report to credit bureaus because it's not a loan. Your credit score remains unaffected whether you use the app once or regularly. This is a major advantage over credit cards, personal loans, or payday loans.

How long does it take to get money from Earnin?

Standard Cash Out transfers take 1–2 business days at no cost. Lightning Speed delivers funds in minutes for an optional fee. Early Pay deposits your full paycheck up to two days early. The speed depends on your bank's processing time and which option you choose.

Is my bank information safe with Earnin?

Earnin uses bank-level encryption and security protocols to protect your information. The company doesn't sell your data to third parties. That said, Earnin has experienced security incidents through partner networks, so monitor your accounts regularly for unauthorized activity and consider a credit freeze if concerned.

Can I use Earnin if I'm self-employed or a gig worker?

Earnin generally requires consistent W-2 employment with verifiable direct deposits. Gig workers and self-employed individuals typically don't qualify unless they have regular income through a connected platform with verifiable earnings. Freelancers and independent contractors should check eligibility directly with the app.

What happens if my paycheck is late or smaller than expected?

Earnin automatically adjusts repayment if your paycheck is delayed. If your check is smaller than your Cash Out amount, Earnin may debit the remaining amount from your linked bank account. Contact customer support if this happens—they can often reschedule repayment or work out a solution rather than taking the full amount immediately.

%201.svg)